Earnings Per Share (EPS) is one of the most widely used metrics in financial analysis—and for good reason. It represents the portion of a company’s profit allocated to each outstanding share of common stock, making it a key indicator of profitability and shareholder value. Whether you’re a seasoned investor, a financial analyst, or just learning the ropes, understanding EPS is essential for evaluating a company’s financial performance.

Table of Contents

What is EPS?

Why is EPS important?

What are the different types of EPS that companies are required to report?

What is basic EPS?

What is diluted EPS?

What are examples of dilutive securities?

How do you calculate diluted EPS?

Why do we use the weighted-average number of shares outstanding in the EPS calculations?

How does a company calculate their weighted-average number of shares outstanding?

What is the effect of Stock Dividends and Stock Splits on EPS?

Do we include anti-dilutive shares while calculating dilutive EPS?

What is EPS?

Earnings per share (EPS) is the portion of a company’s profit over a reporting period allocated to each share of common stock outstanding on a time-weighted basis over that same period. EPS serves as an indicator of a company’s profitability and is calculated as follows:

EPS = Net Earnings Available to Common Shareholders / Weighted-Average Shares Outstanding

Why is EPS important?

EPS is an important metric that investors use to asses a company’s financial performance and equity valuation. It is also used to calculate the commonly-used price-to-earnings (P/E) valuation ratio. By dividing a company’s share price by its earnings per share, an investor can understand the value of a stock in terms of what the market is willing to pay for a dollar of the company’s earnings.

EPS is an important fundamental metric because it breaks down a firm’s profits on a per share basis. This is especially important because the number of shares outstanding could change over time which means that the aggregate amount of earnings of a company on its own is not a good measure of financial performance.

What are the different types of EPS that companies are required to report?

Companies need to report both basic and diluted EPS for all financial periods appearing on the income statement. Basic EPS uses the actual weighted-average number of shares outstanding during the period, whereas diluted EPS considers the hypothetical impact of the conversion of any dilutive securities that are convertible into common stock. Dilutive securities could include warrants, stock options, convertible bonds or preferred stock.

What is basic EPS?

Basic EPS does not consider the effect of any securities that can convert into more common shares and add to the total number of shares outstanding (“dilutive” securities). Basic EPS simply uses the company’s reported net earnings available to common shareholders in the numerator, and the weighted-average number of common shares outstanding during the period in the denominator:

Note that if the company has preferred shares, dividends on these shares will be subtracted from net earnings because EPS refers to earnings available to common shareholders. However, common share dividends are not subtracted from net earnings in the EPS calculation.

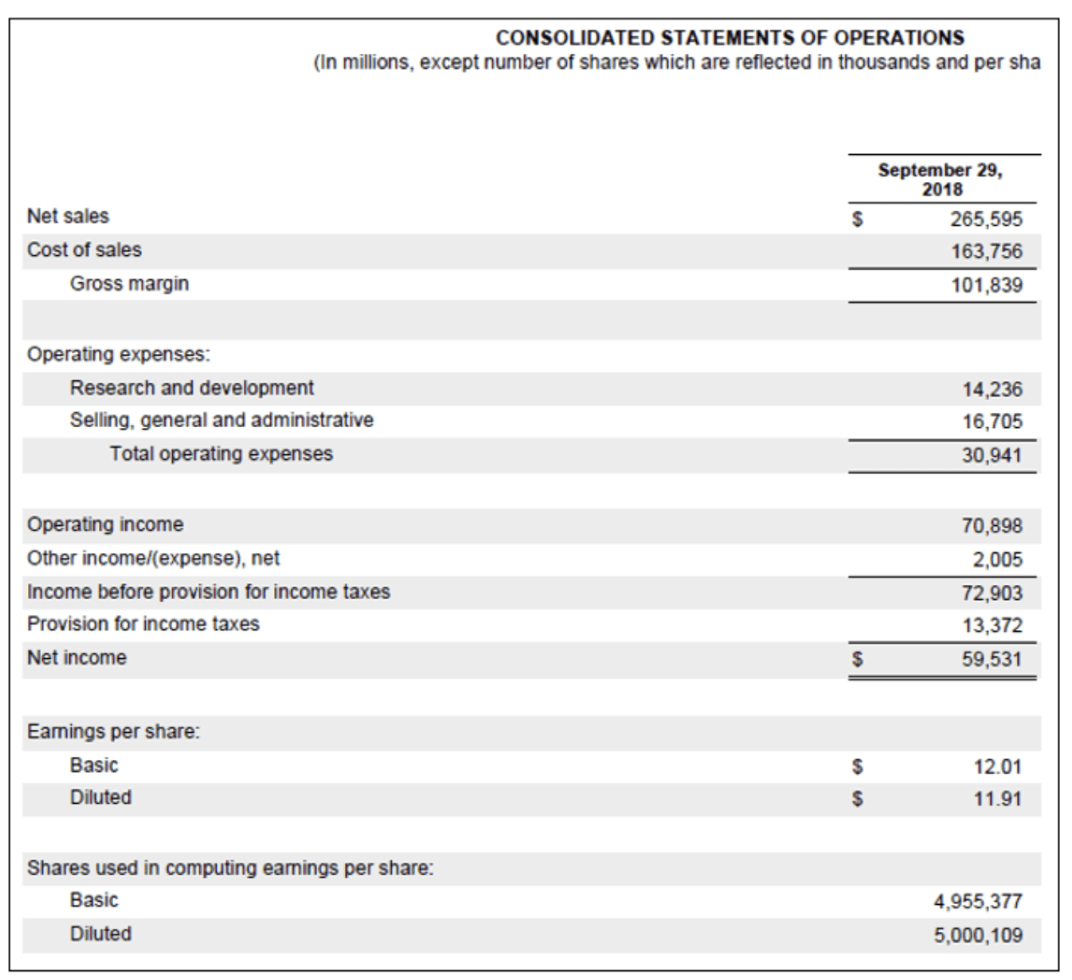

Example: Apple’s Net Income attributable to Common Shareholders for fiscal 2018 was $59.5 billion and the basic weighted average common shares outstanding was 4.955 billion. Therefore, basic EPS for Apple in 2018 was $59.5 / 4.955 = $12.01 / share (see Figure 1 below).

Figure 1: EPS

What is diluted EPS?

Diluted EPS is a hypothetical calculation that shows the impact on EPS if all securities that would lower earnings per share were converted into common stock (such as stock options, warrants, etc.) and added to the total number of shares outstanding. Under most circumstances, research analysts will forecast diluted EPS. Similarly, it’s most common to use diluted EPS as opposed to basic EPS when doing comparables analysis.

Dilutive securities (i) can be converted to common stock if the holder exercises their option, and (ii) would reduce EPS if the holder of the security converted their security into common stock.

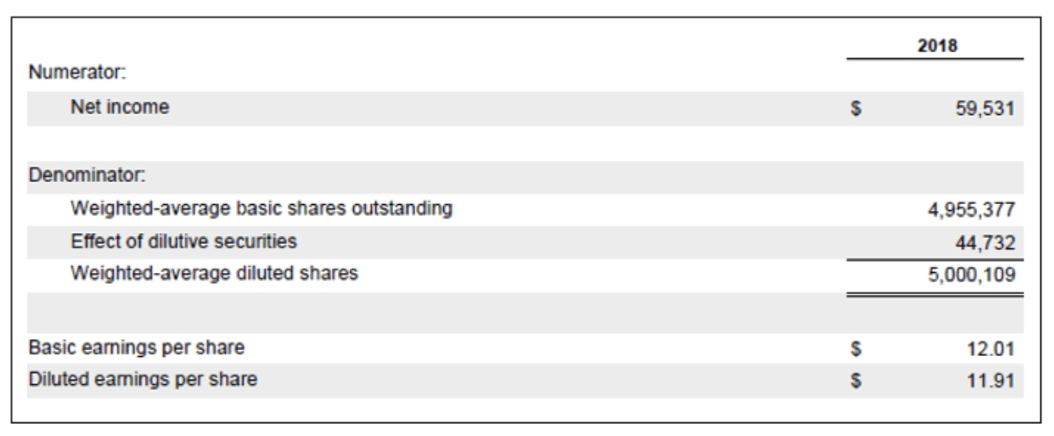

In Figure 2 below, we see that an extra 44.732 mm shares are included in Apple’s diluted share count but there is no adjustment to net income:

Figure 2: EPS

What are examples of dilutive securities?

Stock options, warrants, restricted stock units (RSUs), convertible debt, and convertible preferred shares are common types of dilutive securities.

- Stock options and warrants grant the holder the right to purchase common stock at a set price for a set time.

- Restricted stock units grant the holder common shares when they vest.

- Convertible debt allows the holders and/or issuer to convert the debt into a specified number of common shares at specific times.

- Convertible preferred shares allow the holders and/or issuer to convert the preferred equity into a specified number of common shares at specific times.

How do you calculate diluted EPS?

For historical periods, in most instances we don’t calculate diluted EPS because public companies always disclose diluted EPS in their annual and quarterly filings.

However, if it’s necessary to calculate diluted EPS (i.e. in a forecast model), two adjustments need to be made:

- Increase the weighted average number of shares outstanding assuming dilution occurred at the beginning of the financial reporting period; and

- If needed, adjust net income to common shareholders to give pro forma effect to the conversion into common shares – for example, if the convertible preferred shares are dilutive, we would need to add back any preferred dividend to net income.

Why do we use the weighted-average number of shares outstanding in the EPS calculations?

The weighted-average number of shares is used in the EPS calculation to match the fact that the income in the numerator is earned over the reporting period. In other words, a common share only begins to share in the earnings of a company on the day it becomes outstanding. By the same token, a share that is repurchased ceases to participate in the earnings on the day it is bought back by the company. Because of the detail needed to calculate weighted average shares outstanding, the company provides this number and publishes it in its financial statements and notes.

How does a company calculate their weighted-average number of shares outstanding?

The weighted average number of common shares is the number of shares outstanding during the year weighted by the portion of the year they were outstanding.

There are three steps to calculate the weighted average number of common shares outstanding:

Step 1 – Compute the number of shares outstanding after each change in the common shares. An issuance of new shares increases the number of shares outstanding whereas a repurchase of shares reduces the number of shares outstanding.

Step 2 – Weight the shares outstanding by the portion of the year between one change and the next change. Weight = days outstanding / 365 = Months outstanding / 12

Step 3 – Sum up to compute the weighted average number of common shares outstanding.

Note that the weighted average share amounts, both basic and diluted, are typically disclosed either directly on the income statement, or in the notes and/or MD&A. The implied number of shares can also be calculated by dividing net earnings by the EPS.

What is the effect of Stock Dividends and Stock Splits on EPS?

When a stock dividend or split occurs, calculating the weighted average number of shares requires restatement of the shares outstanding before the stock dividend or split. It is not weighted by the portion of the year after the stock dividend or split occurred.

If a stock dividend or split occurs after the end of the year, but before the financial statements are issued, the weighted average number of shares outstanding for the year (and any other years presented in comparative form) must be restated.

Do we include anti-dilutive shares while calculating dilutive EPS?

An anti-dilutive security is one that causes the earnings per share to INCREASE or the loss per share to DECREASE. Some potentially convertible securities are anti-dilutive which means that their inclusion in the EPS calculation would result in an EPS which is higher than the company’s basic EPS. Under both IFRS and US GAAP however, these anti-dilutive securities are excluded from the calculation of diluted EPS.

In other words, as a rule diluted EPS should always be less than or equal to basic EPS, and should reflect the maximum potential dilution from the conversion of potentially dilutive financial instruments.

Diluted EPS is a potential worst-case scenario and hence cannot be higher than basic EPS.

Learn more with Training The Street

If you enjoyed reading this article and want to improve your Excel Skills further, then why not try our Excel Best Practices for PC Self-Study Course. You can also browse our other range of Self-Study Courses here.

Training The Street also offers a more advanced In-Person/Virtual Public Course called, Applied Excel where you can gain the skills needed for parsing, analyzing, and presenting information from large data sets.