The following three statements are all true:

- In November 2019, Hertz went out to investors asking for $750M. Investors, impressed with what they saw, gave the company $900M instead.

- In April 2020, four billion dollars of Hertz’s debt was rated triple-A, the same rating that the US government gets for its debt. Triple-A is as money good as it gets in this world.

- One month later Hertz went bankrupt.

What happened?

In 1918, a 22-year-old entrepreneur named Walter Jacobs began renting a fleet of twelve Ford Model-Ts in Chicago. His business caught the attention of John D. Hertz who, in 1923, acquired the company and began operations under the Hertz name. By 1925, Hertz built a coast-to-coast rental network generating about $1 million in annual revenue.

Fast forward about a century, Hertz now rents more than 770,000 vehicles. It operates from 12,400 locations in North America, Europe, Latin America, Africa, Asia, Australia, the Caribbean, the Middle East and New Zealand. It owns Dollar and Thrifty. It’s huge.

And that’s the Hertz which raised $900M from the debt markets back in November. Here’s what Moody’s had to say about it:

Hertz has made notable progress in strengthening its corporate governance framework with respect to accounting controls, technology and information systems, and establishing a senior leadership team. In addition, it continues to embrace a prudent financial strategy in the face of large and ongoing needs to access capital markets (emphasis ours).

Translation: It’s all good. Hertz is big so it needs a lot of money. It will get the money it needs.

Hertz was big. But was it safe?

The two most common metrics for safety are leverage ratio and coverage ratio. Here’s our instructor, Van Vu, describing these ratios in our Financial Statement Analysis module.

Hertz’s leverage and coverage ratios at the time were 9.7x and 2.5x respectively. Historically, that would make a firm extremely vulnerable to a recession. But no one was really predicting a recession back in November.

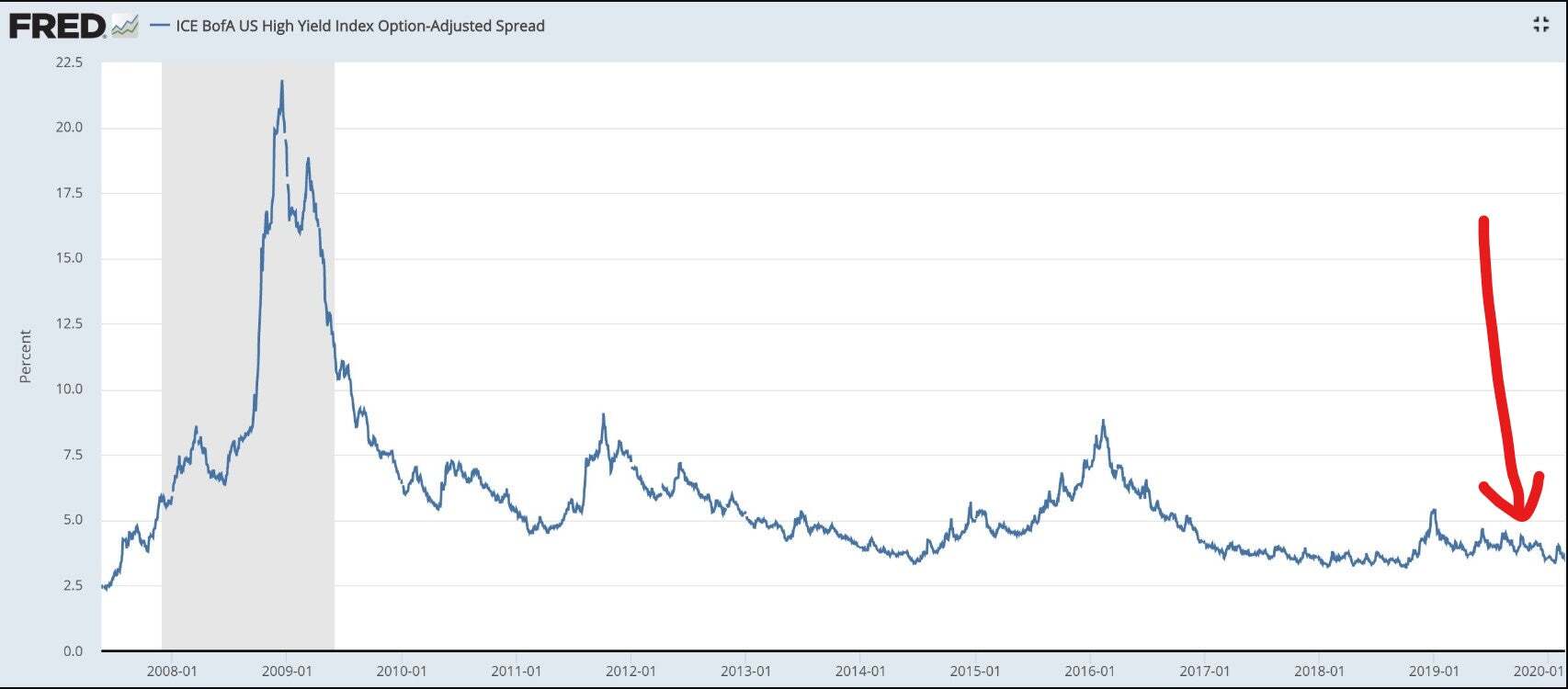

Here is what the credit markets looked like pre-Covid.

This is the spread that a borrower like Hertz would have to pay over-and-above the US government interest rate. In November the spread was 4%, around the lowest it had been in 12 years.

This meant that Hertz could borrow at 4% plus the US government rate of 2%. And that’s what Hertz did. Nine hundred million dollar times over. This debt was rated B3 – not good, but not awful either.

And, what about the triple-A rated debt?

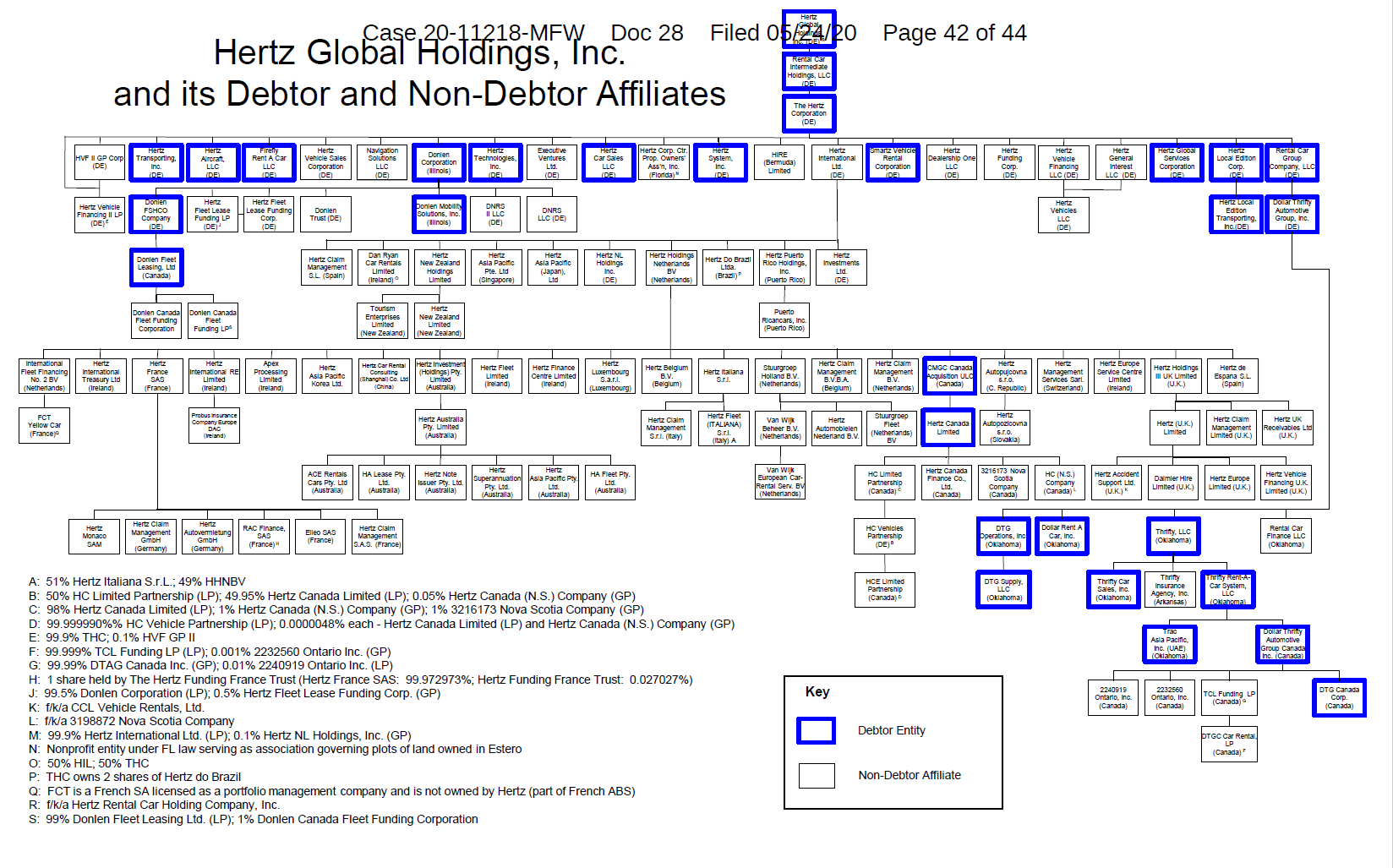

To get to the bottom of that, let’s look at Hertz’s corporate structure. First, the real one, and then a simplified version.

The following diagram comes straight from Hertz’s bankruptcy filing. It’s real but it’s not pretty.

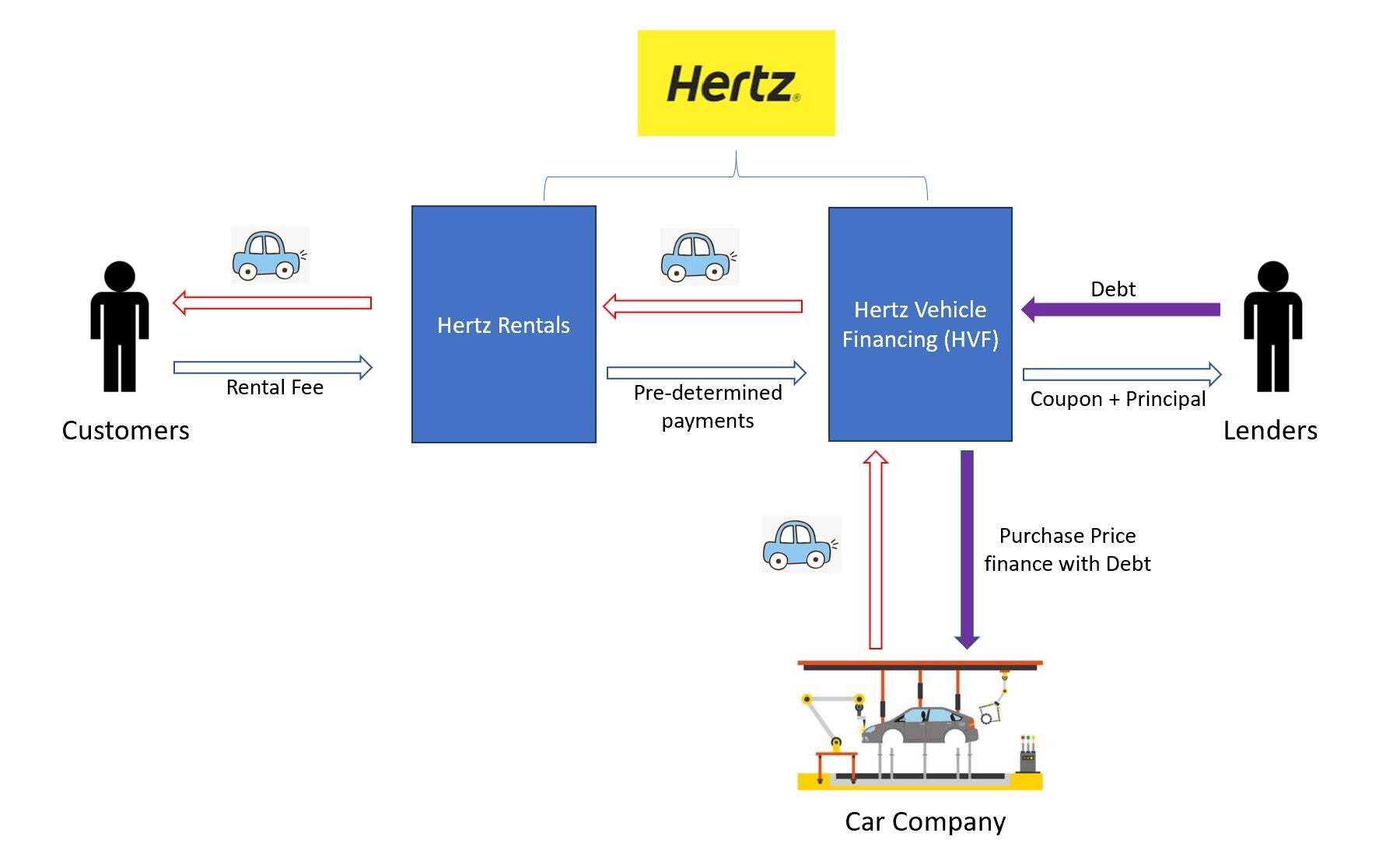

Here’s our simplified version.

Hertz is an agglomeration of two companies, Hertz Rentals and Hertz Vehicle Financing (HVF). HVF buys the car using debt. It then leases the car to Hertz Rentals. And, Hertz Rentals rents the car to us.

The money flows in reverse. Hertz Rentals gets paid whenever the customer pays. But Hertz Rentals has to pay HVF on a regular basis, regardless of how the business is doing.

This, in theory, makes HVF cashflows more predictable than Hertz Rental cashflows.

Additionally, and more importantly, HVF debt is secured with all those cars in the fleet. If the payments ever stopped, the lenders can seize the cars.

But that’s not all. Remember, these cars depreciate fast. Hertz protects the HVF lenders against that eventuality as well.

Here’s Hertz describing this arrangement in its bankruptcy filing:

The Company currently operates a rental portfolio of approximately half a million vehicles in the United States (many of which are now sitting idle due to Coronavirus). In the United States and certain other jurisdictions, the Company finances its fleet of vehicles through ABS Programs such as HVF. In general, under the ABS Programs for the Company’s rental fleets, the Company pays monthly scheduled depreciation, but must also pay into the financing structure an amount corresponding to estimated market depreciation in order to prevent a reduction in its access to funding.

Translation: Hertz has to pay HVF for depreciation. And has to pay extra for extra depreciation.

All of these protections together made the HVF debt super-safe. And all of these protections made Hertz super-unsafe.

When Covid hit, not only did the business go down, but so did the value of used cars. And as specified in the contract, HVF lenders came knocking on the door asking for that extra depreciation. They wanted $135M in cash. Hertz did not have it. So on May 27th it filed for bankruptcy protection.

Hertz is now going through the courts, devising a plan for revival, and getting all its lenders to agree on the plan. To keep up with further updates visit this page.

Oh, and those bonds that were going to pay $54M in coupon every year, and pay back the $900M in 2028 …

Those bonds are on their way to joining the extremely distinguished “No-Payment-At-All” club.