Failure of Regulations or Regulator?

Many words have already been written about the failure of Silicon Valley Bank (“SVB”): the causes, the implications, whether there should be a Government bailout, should Glass Steagall be reintroduced – even should the FDIC deposit insurance be increased from $250k to $20m!

To add to the mix, I want to discuss the implications for banking regulations – in particular Basel 3. Having started my career as a financial trainer in 2009 after the global financial crisis (“GFC”) helped end my banking career, I have spent thousands of hours training this very topic from Singapore to NY and from Edinburgh to Johannesburg. While the Basel 3 rules are not perfect, I do believe they are fit for purpose. I do not think that the failure of SVB is due to banking regulations – rather banking regulators, or specifically the Federal Reserve Board (“FRB”).

What causes banks to fail?

Banks can fail for many reasons; however, they do tend to have the following in common: a negative event or piece of news scares the market, depositors start to withdraw money, further investigations see that the bank has poor liquidity or insufficient capital, this reduces confidence and this causes depositors to panic causing a run on the bank.

Basel 3 was meant to prevent liquidity issues…

Under Basel 3, a global regulation was introduced to cover this exact situation. The Liquidity Coverage Ratio (“LCR”) meant that banks are required to have enough high-quality liquid assets (“HQLA”), including Government Bonds and MBSs, to cover a liquidity event. Banks need enough HQLA to sustain 30 days of net cash outflows (deposit withdrawals or funding maturities). Individual sources of funding are prescribed run-off rates based on how much funding is likely to disappear in a liquidity event. Long term funding is excluded, as this clearly is outside of a 30-day window; but the short-term wholesale funding (interbank) whose overreliance helped cause the GFC was effectively eliminated as a viable core funding base.

The focus became much more about banks creating a stable deposit base to fund their loan portfolio as these deposits tend to act quite sticky, although technically they are on-call. As an example, banks such as Barclays in the UK have gone from having a Customer Loan to Deposit ratio of c.130% in 2009 to c.70% in 2022, meaning that its whole loan book is more than funded by customer deposits.

The prescribed run-off rate for a stable retail deposit (those covered by a deposit insurance scheme) is 5% (and 3% in some instances) and 10% for a less stable deposit. Corporate deposit run-offs are 25% for a deposit with an “operational” relationship and 40% for a “non-operational” relationship. For the amount covered by the deposit insurance the run-off is only 20%. Often small corporates will be considered a Small and Medium Enterprise and be covered by the retail deposit run-offs.

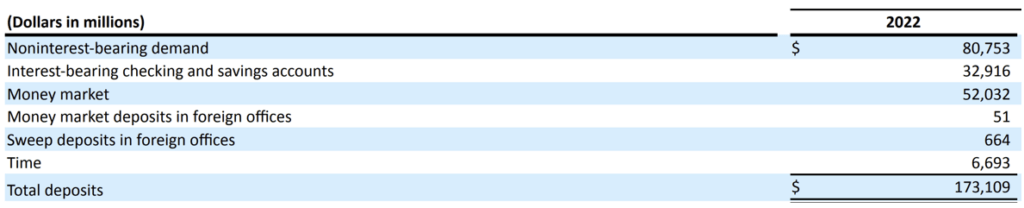

Looking at the recent 10-K, SVB had total deposits of $173b: of this amount $52b were money market (interbank) accounts, the majority c$120b were customer deposits. Normally, you would consider this to be quite adequate as SVB had only $72b of loans and $120b of liquid assets.

First failure – Unmonitored Duration Risk

While we are on the topic of those liquid assets, this is the first regulatory failing. Investing deposits into fixed income instruments is not a controversial decision – this is a key part of what a bank does. However, SVB took significant interest rate and duration risk in making these investments in Government Debt and Mortgage-Backed Securities. The assets themselves are relatively low credit risk, but as most of these assets had maturities greater than 10 years they have high duration risk, where they are highly exposed to interest rate changes. It is the excessive unhedged duration risk that was the greatest concern. On page 147 of the 10-K you can see that SVB reduced its interest rate swap exposure from $10b in 2021 to $0.5b in 2022.

This is an area that the regulator should have stepped in – to discreetly ask them to either reduce its duration risk, or issue more capital to cover the potential risk. This is what is called Pillar 2 intervention, regulators have this power, and use it regularly in Europe.

Second failure – Regulator Waives the Rules

The second regulatory failure is that according to SVB’s annual report they are not subject to the LCR. For a bank the size of SVB to not be subject to one of the key Basel 3 regulations is alarming. Not only should SVB have been subject to the LCR, but they should also have had to voluntarily report details on its liquidity position under Pillar 3 reporting obligations for the investor (debt and equity) universe to provide additional market discipline. These regulations do exist – but the regulator chose not to implement them. In the US the FRB have opted for 5 levels of supervision but SVB were category 4 (5 being the lowest). In Europe, all banks must complete Pillar 3 disclosure and report its LCR.

Third failure – Vacancy: Chief Risk Officer

The third regulatory failure was around corporate governance. SVB did not have a Chief Risk Officer (“CRO”), who resigned in April 2022. Risk committee meetings doubled in 2022 which suggests the Board of Directors had concerns. This should have been an additional red flag for the FRB.

Fourth Failure – Deposits Wanted: Tech Millionaires Need Only Apply

While SVB was not formally subject to the LCR, I would hope that the bank and regulator would at least be calculating this or other measures to at least monitor SVB’s liquidity position. Even if we mark down the value of the liquid assets, the LCR ratio would probably not have been too bad. Remember, its depositors are made up of retail depositors and corporates who I imagine have operational relationships with the bank. The run-off for those types of deposits is low: 3%, 5%, 10%, 20% and at worst 25%. However, the biggest regulatory miss in my opinion is something that SVB voluntarily disclosed on page 80 of its 10-K.

Of its total c.$173b of deposits, only $21.5b were covered by the FDIC. Meaning these were not millions of customers with thousands of dollars on deposit, these were thousands of customers with millions on deposit. That is a level of concentration risk that any regulator should find unacceptable. Again, this should have resulted in a very awkward chat between the CRO and the regulator who would have placed additional liquidity requirements e.g. issue long-term bonds and perhaps additional equity for good measure.

Potential Solutions

The light-touch regulatory approach has led to a much more profitable US banking system compared to Europe. This has resulted in US banks trading at higher valuation multiples, but at the cost of a failed bank. The question now is what happens next? Any kind of public bail-out would be unpopular given the demand for much tighter regulation. It would seem more logical that the US banking sector bail out the bank through one of the larger banks acquiring SVB at a discount to its (questionable) book value, in the same way that HSBC acquired SVB’s UK assets.

My final comment is how much bank failure is acceptable? How much should we rely on the regulator? Alternatively, how much onus is on the investment industry to regulate. A bank might discontinue its risky undertakings if its share price gets priced down, or its bond yields spike accordingly. Are analysts in the US trained in specialized bank analysis to the same extent as their European counterparts?

The answer is no.

Training The Street is the largest trainer of technical skills for investment bankers in the world. We run thousands of corporate finance courses in the US and Globally each year. However, our specialist FIG courses, the ones that specialize in analyzing banks like SVB (financial statement analysis, financial modeling, valuation, M&A and regulatory capital) are far more in demand in Europe, Asia and Middle East, than they are in Americas. Considering the failure of SVB, maybe that needs to change.

If you are interested in running specialist bank analysis courses contact us at [email protected].